Personal Finance

This is all the stuff you wanted to learn in school; its practical, and you shouldn't be confused by 401ks, taxes, and investments.

- Overview of Personal Finance

- Rights at Work

- Rights as a Customer

- Negotiation

- Taxes

- How Retirement Accounts Work (401k, IRAs)

Overview of Personal Finance

Everyone is trying to take each others money, its important you don't fall in this trap and that your hard earned money is kept for yourself. Beyond this, its important to know how to passively grow your money and have access to all the tools the rich people use.

If you are learning more for a step by step guide on what to do when you need to stretch your money, reddit has a great guide on this. My goal here isn't to teach you how to make it a budget, you probably already know you shouldn't buy that pumpkin spice latte, but I want you know how the system works so you are better armed throughout life.

https://www.reddit.com/r/personalfinance/wiki/commontopics/

The very very first step is to learn how to not get ripped off. Yes you don't want to fall for scams, but its also about knowing your rights. Landlords can try to keep your money or make up bogus charges, hospitals will make up costs all the time, employers will try to steal your time and short change your paycheck. Making sure you don't have your rights infringed on is extremely important to getting the money you are entitled to.

This ties very closely to another topic that is critical to finance: negotiation. This one blew my mind in college; I never realized prices at grocery stores and car dealerships are literally made up, there is no such thing as a set in stone price, and if anyone says "well the price is the price" is full of shit. Likewise, how much you get paid works the same way. However, negotiation isn't the art of sounding cool and yelling at people, its a game of knowledge. Prices are made up, but they don't come from thin air, they come from the expectation of what they think people will pay for them, and wages come from what employers think employees are willing to suffer through. Academically, we call these "market forces". If you can understand the forces affecting a price, and you have some confidence in this understanding, then you can know when you are getting ripped off and when you can get a better deal. The negotiation article will talk about this and BATNA, "best alternative to negotiated agreement", which is what you will do if you can't agree on a deal/price. Increasing the value of your alternatives strengthens your position. Likewise, being aware of your opponents BATNA lets you know how desperate they are. AVOID DESPERATION, that is how people get you! You are willing to pay more for rent than you should because you are on the verge of being homeless. You will accept terrible working conditions because you have kids to feed.

Now you that you've studied basic rights, how markets and negotiation work, now its time to learn about the machinery of finance. You'll want to learn about taxes, high interest savings accounts, retirement accounts, 401ks and IRA, the stock market, credits cards, credit scores, loans, and perhaps LLC formation if you are interested in running a business.

Finally, this gets all tied together in learning how to do a discounted cash flow. You HAVE to know how to do this. College grads with MBAs (masters of business administration) think they are all super smart because they can make this in excel, its super easy. In short, it evaluates the money you put into something (an investment) by comparing it to another investment (essentially your BATNA for money). This is how all the big money people, wall street, real estate companies, etc, will evaluate their investments. You should do the same thing. The key assumption here is "the time value of money". Think about it this way, if I promise to give you 100 dollars today, or 10 billion dollars in 200 years, which offer will you take? You better take the 100 now because you'll be dead in 200 years! Now the question becomes, would you rather take 100 dollars today or 100 dollars in 3 weeks. Obviously you'll take the money now, why have it later when you can have it now? You can put that money in the bank and get interest, even if minor, in 3 years. Now we gotta evaluate the real question, would you rather take 100 dollars now or 110 dollars in a year? Will your money in the bank grow to 110 in a year? Probably not. Will it grow that much in the stock market? Maybe? The key point here is money is worth more now than later, and if you have to wait for your money, you better be compensated for it. Of course, there are other items you have to look at. Can you use that 100 bucks to buy a sweet sweet video game that you will enjoy? Why tie up money in investments when you can live life? Be armed with these tools, then make the decision yourself.

After this I might make some fun articles zooming out from personal finance and explain some basics of how the american financial system works, i.e. where money comes from and what tools we use to keep the economic engine chugging. It is important with respect to bond markets.

Rights at Work

Rights at Work

The very first people that will tell you complete and utter bullshit in hopes they can take more money from you is your employer.

Some common ways employers try to screw you

1. Wage Theft: If you are working, you have to get paid, this includes meetings and trainings. If they tell you to show up 30 minutes early to go over some company policy, they need to pay you for those 30 minutes. If they close the store but you are stuck cleaning the place up, you have to get paid for that. They do not have to pay you for a lunch break. Some states have more strict rules than others, i.e. new york is better than florida. If you suspect wage theft, speak up.

2. Making employees pay for business expenses: Employers are allowed to have a dress code, i.e. make you wear a generic black shirt, but if your uniform has a company logo or is specialty equipment, the employer must pay for that. They get to write it off of their taxes as its a business expense, so it doesn't even cost them much. Do not pay for anything thats a business expense.

3. Rules against discussion wages/salaries: It is illegal to tell employees they can't discuss their wages. You are allowed to freely discuss what you make. There could be some rules against spending work time doing this but you can do whatever you want on break and after work.

4. OSHA: The occupational health and safety act guarantees a safe workplace and employees do not have to do work that is dangerous and cannot be fired for doing so. Furthermore, employees are free to report unsafe work conditions to OSHA without fear of retaliation.

5. Protected Classes: This one might be more state specific and I am most familiar with New York: in New York you cannot be fired for being pregnant, for being old, for being black, for being gay. Employers will lose in court if they cannot prove employees were fired for other causes. A clear cut case is an employee announces they are pregnant and 3 days later the employee says they are going through layoffs and they were cut off. Unless the employer had CLEAR documentation you were being laid off before being told about the pregnancy, they will lose in court and you can sue for damages and lost income and lawyer feeds.

The more money you make and the easier you can get another job, the easier it is to fight your employer. I only say this because the united states generally has "at-will employment", which means you can quit for zero reason and employers can fire you for zero reason. That being said, employers cannot fire you for certain reasons, such as being pregnant or complaining about certain safety conditions. If they fire you after one of these certain reasons is present in you, then they basically have to prove they didn't fire you for that reason, otherwise an employment lawyer will eat them up.

The most likely employer to break the law is a small mom and pop shops; so you work for your uncle's friend, he and 4 dudes mows lawns. Employment lawyers won't want to target him because he doesn't have that much money to sue for. If you work for a large company like wal-mart, you can almost guarantee they take a large effort to follow the law because anytime something is violated, you can get a free consultation and lawyers will be salivating to sue them for everything they got. Lawyers might be expensive and annoying, but they are critical to ensuring a fair and compliant society in the United States.

Rights as a Customer

Hospitals

DO NOT PAY YOUR HOSPITAL BILLS. They will make up costs and try to pressure you into paying crazy bills, sometimes thousands of dollars. Never pay these. Just wait, discuss the price with the hospital (be nice) and your insurance company. And then wait some more. They will eventually pass these to collections and sometimes if its small, it will go away altogether. It could take a hit on your credit, but they will not sue you for a small bill, and if you can't afford the hospital bill, you probably aren't taking out a home loan where your credit score matters.

Death of a Loved One

DO NOT PAY THE BILLS OF YOUR DEAD PARENTS. Unless you are a cosigner on a loan, debts belong to the debtor and the banks factors that risk when giving a loan to someone. Companies will try to come after people's children to pay for the credit card bills or other bills of their parents and grandparents. They are scamming you and you don't owe them anything. If someone passes a way, everything they owned is called their "estate" and the estate will owe money. Once the estate pays out its debts, then the remaining money can pass on to next of kin or however defined in their legal will.

Your Landlord

If you rent, you own nothing in the apartment; if it came with lightbulbs, those lightbulbs belong to the landlord. Do not fix your landlords stuff for free.

In New York, there are tons of tenant protections. They cannot remove you from the apartment if you have been there for more than 30 days without winning in eviction court and having the sheriff come and forcibly remove you. It is illegal for them to change the locks and you can call the police on them. I only mention this because landlords try to do stuff like not fixing the heating, or not addressing mold. You can withhold rent for unsafe living conditions and if you do that it takes them at least 6 months minimum for them to kick you out. Learn the rules in your state.

When you move out, they might try and take money from your security deposit. In New York "normal wear and tear" is allowed, which means stuff can break if its old, do not let the landlord use your security deposit to fund their upgrades. You can take them to small claims court and you will probably win. The more people do this, the more landlords stop taking advantage of tenants.

Utilities

Never give anyone your utility account number, there are a bunch of fake green companies trying to sign you up for special energy. It is a scam and they will claim you are buying green energy for your apartment and then double your bills for that. Never never sign up for these things.

If you see "estimated bill" on your utility bill, that means they are making up a number because they can't access your electric or gas meter. You can take a photo of your meter and send that to them, or schedule a person to come and read your meter. Utilities will often overcharge on these estimates and can do it for years.

If you suspect your bill is too high, sometimes a landlord will have the wrong meter assigned to you, or they'll have your electricity tied in with the main hallway. Testing this with electricity is really easy, kill all the breakers in your apartment and see if the hallway lights go out or if someone else's apartment loses electricity. Gas can be tough, its worth asking to look at the meter.

Sometimes your electric bills will be crazy high in the winter. you might have rented a place with electric resistance heat. It is the most expensive form of heating, heat pumps are fine, resistance heat is BAD. Ask about this when you shop for an apartment, otherwise you'll be getting $400 dollar a month electric bills. If you do get caught in this situation, try lowering your thermostat or turning off the heat at night and sleep with an electric blanket.

Negotiation

People tend to think of negotiation as a game of charisma, if you can just be persuasive or forceful enough, you can strike a better deal, get more for less, etc etc. In reality, it is a game of knowledge, power, and some guesswork.

I did an internship when I was 21, and the manager was nice enough to give us a mini MBA course as part of the internship. It blew my mind that literally everything can be seen as a negotiation. There is no such thing as a fixed "price" for anything. Even what you get paid is ultimately a negotiation. This isn't very profound once you have this knowledge, but as a kid raised by parents who grew up very poor, were generally risk averse, and didn't understand large complicated systems that ran society, this was a game changer. So with this in mind, lets get to the fundamentals of a negotiation, settling on price for something.

One definition we'll talk about up front. BATNA: Best Alternative to negotiated agreement. This is what you do if you can't settle on a price, or an agreement in a negotiation. Its very important for assessing your power in the negotiation, and how far you are willing to push it.

So lets saying you really want to go a taylor swift concert (but its 2008 so the prices aren't crazy and she ain't so famous yet), but either through you being dumb and forgetting to get a ticket until the night before the concert, or because there are a bunch of scalper assholes out there snatching up the tickets, you find yourself outside the stadium trying to get a ticket. What proceeds is a battle between you an the scalper to negotiate a price of the concert ticket.

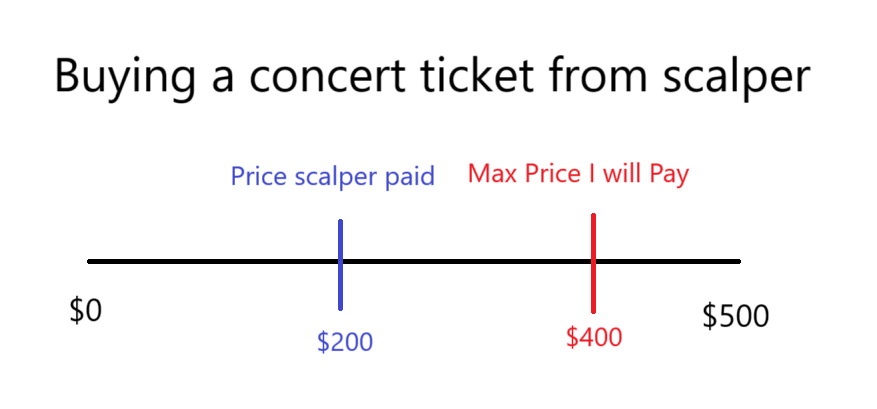

The scalper says he will sell you a ticket for $500 dollars. If you are not privy to negotiation, then the price is the price and you have to make a yes/no decision on this. You check your wallet, you only have $400 dollars cash. Even if you had more, you think you'd rather put $401 dollars to fufill your dying wish of having a playstation 3 that costs $599 US dollars.

But lets not give up, remember, this is a game of secret information. How much did that scalper pay for the ticket?

Oh well look at that. The scalper is making money even if they sell it for $250 dollars. In simple situations, this will be called ZOPA or Zone of Possible Agreement. In academic terms, this is where the final price should lie, and where you land here is a battle of risk taking and confidence. As you'll see, 200-400 isn't necessarily the zone of possible agreement here. But if you were putting in a new order for laptop or some manufactured good, you'd need to above their cost of making the good (its actually a little more complicated than this, you'd technically need to be above their variable cost).

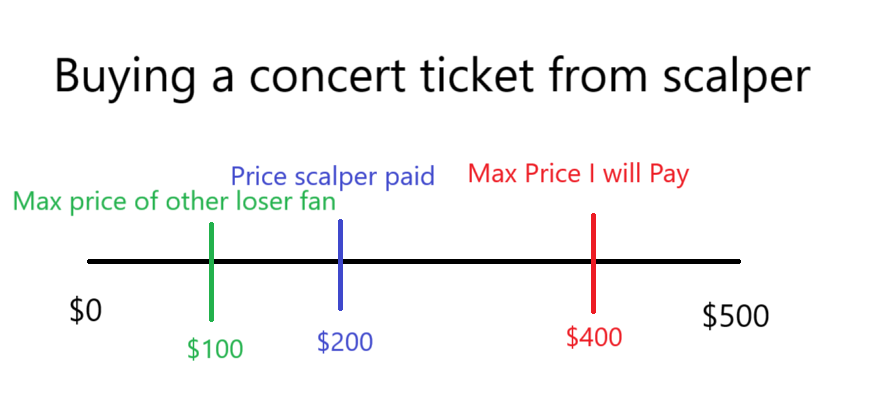

You think about making an offer to the guy. That Playstation 3 can wait, being a swifty cannot. But then this confidence leads to even more confidence. You start thinking... what if the scalper can't sell any of his tickets? Once the concert is over, those tickets are worthless, and the asshole scalper lost $200. Even if he sells it for $5, he is still better off than selling for $0.

So you wait, and wait. The crowd roars as taylor swift comes on stage. At this point you take a deep breath, and go to offer the man $5. But someone beats you there.

What a loser! They offer the guy $100 dollars. And so the bidding war begins. You realize there are no other scalpers out there. You remember you have terminal cancer and this is your last time you can see taylor swift before you die. You tell this to the scalper in hopes that he will lower his price for you. Instead, he doubles down, being an asshole scalper, and asks for $500 dollar for the ticket. Fortunately, the other bidder was a rich european tourist who happen to be in town for the concert and had nothing better to do than tickle his desire for the thrill of negotiating, gives you $100 bucks, and you pay the scalper $500 for a ticket you said you were going to walk away from at $400 dollars. FOMO is real, especially when YOLO is real.

Lets break down a few things that happened here.

-

Being desperate ruins your negotiation power. If your BATNA (best alternative to negotiated alternative) is to never see taylor swift in your life and save towards a PS3 you might not live to play, then you set yourself up for price gouging. This is particularly bad for people that are poor and have important things to do. For example, someone who is jobless might accept a very low salary because they have a kid to feed. Likewise, if someone is struggling to find a job that will sponsor a visa, they might accept well below market rate just to stay in the country.

-

Some sellers will hold firm because they don't want to train a certain behavior. Lets say there was no second buyer, and you were literally the last person willing to buy a ticket for $5? Sure, its better in the moment for the seller to take $5 instead of no money, but what happens when you post this on the internet, then everyone is pushing for that kind of deal? The scalper might just take the $0 and establish a hard line that they won't negotiate with such an offer so far from asking price. Theoretically this is worse for the scalper, especially as future buyers can bid to drive each other's pricing up, but a small group of fierce negotiators can wear down a general public of weak negotiators.

- Increase your information to improve your negotiation. Knowledge is power, and you won't know what the scalper paid for his ticket, but you can have a pretty good guess.

- Improving your BATNA is key to getting the best outcomes. You get the best deals if you hold firm. But this also increases the change the entire deal will fall through. This means that having a better BATNA is key to getting good pricing and good salaries.

How to improve your negotiation skills?

In every negotiation you can take the time to gather the needed info, do the math on where you think the over

Taxes

We give up the freedom to keep every dollar we earn in exchange for having a military that defends us against foreign invaders, a police department that catches criminals, funding of institutions that discover new science, and much much more. No one doubts we need these things, but people are unhappy that god forbid they have to be the one that pitches in for a society that follows rules and maintains roads.

In order to get around the human nature of not wanting to contribute toward the common good, the people that run the world have figured out many ways into forcing assholes to pay their fair share to the government. The one you are most likely to see are sales taxes, which is a stupid policy and adds 2-10% to most things you buy, you aren't required to do any paperwork for this so that isn't what this article is about. There are also property taxes for people that own land and buildings; you are too poor to own property and buildings otherwise you wouldn't be reading this article. And then there are INCOME TAXES, which every other country does for you but in America you have to figure out how to do it yourself, then the government sends you to jail if you do it wrong after they double check your work.

So with those stakes, lets get started.

What people don't realize is you can easily do your own taxes and mail it to the IRS (Internal Revenue Service). This is done through IRS from 1040. If you go to the link below, you will find the form, and more importantly, the form INSTRUCTIONS. Read the instructions at some point so you get how the websites work.

https://www.irs.gov/forms-instructions

If you make less than 60k a year or something, you don't have to pay to use most tax websites (except turbotax and hr block, they were mad the government made their own tax software so they took away their free file services. Fuck them. Never use them.)

https://www.freetaxusa.com

I use freetaxusa. IRS also has a few others that will file your taxes for free.

https://www.irs.gov/filing/irs-free-file-do-your-taxes-for-free

So what actually happens? Well you owe taxes to the united states government, and possibly the state you live in (texas and florida are the land of the free and have no income taxes, and it really sucks to live there if you are poor. New York, Illinois, and other civilized places have income taxes). Make sure you pay both. If you live in new jersey and work in nyc, you owe some taxes to both.

The united states federal government collects income taxes and some payroll taxes.

Income Tax

Some people think if you make more money, you can get taxed so much that you actually take home less money. These people are misinformed, you will always take home more money the more you make. This is because we have TAX BRACKETS! So it works like this

0-20k: No taxes

20k-40k: you pay 5% of this money

40k-60k: you pay 15% of this money

60k-150k: you pay 20% of this money

150K+: you pay 30% of this money.

So if you made $50,000 dollars last year, the first 20k isn't taxed. Then the 20k you made after that is taxed at 5%, then the last 10k you made is taxed at 15%. So 5% x 20k = $1,000 and 15% x 10k = $1,500, so you owe $2,500 in federal income taxes.

Now it isn't this easy. There are lots of programs that government has to save you money on your taxes, most of these are "tax deductions", which lowers the income you used to calculate your taxes. So if you have a $5,000 tax deduction, that means you subtract that from your yearly income, so $50,0000 - $5,0000 = $45,000, so you calculate your taxes as if you made 45k. This is different from a tax credit, which straight up reduces the tax you owe. So if you have a $5,000 tax credit, you still calculate your taxes as if you made 50k a year, but then you subtract $5,000 from the final result. So you originally owed, $2,500, then you subtract the 5k tax credit, so now you owe -2,500. Wait thats negative, so the government owes you money? Yes they do. Thats why the child credit is really important.

Okay so I just pay the government at the end of the year? WRONG. Your employer is legally required to withhold money from your paycheck (unless you are a 1099 contractor, which sucks, you have some paperwork and learning to do if your tax document says 1099 instead of w-2). So you actually end up paying taxes out of every paycheck so the government has a consistent source of revenue. When you calculate your taxes, you compare the money you owed with how much you already paid, and then you pay the difference. You'll often overpay, so you get a refund when you file your taxes! You can adjust your withholding with your employer (they uses numbers, either a 0,1,2). Some people don't trust themselves with money, so they want to overwithhold and get an extra payday. The smart decision is withhold as little as possible so you can put that money in a high interest savings account, then owe money in tax season.

How Retirement Accounts Work (401k, IRAs)

You might hear the term from time to time, "did you put money in your 401k this year?". "Did you max out your IRA?". Maybe you've never heard of these terms. Maybe your employer doesn't even offer you a 401k. For that reason, you absolutely should read up on what they mean!

In the United States, we pay something called "capital gains tax" on investments. Selling stocks, houses, and crypto is typically taxed at 15%. (but you have to own it for at least a year, if you sell within a year, its taxed as if its regular income).

What makes retirement accounts special is that you don't have to pay capital gains tax. The downside is you generally can't access this money until you are 59 1/2 years old. The 401k can be especially good because many employers match a part of what you put into the 401k (they'll say something like "we will add $1 for every $1 you contribute, until it hits 1% of your income. So if you make 100,000k a year, you need to contribute $1,000 dollars and then they'll add $1,000. This is money you have to take advantage of and consider with your job offers!)

The government encourages this because they don't want you to be poor when you are old. Social Security will not be enough for most old people, it should be thought of as a backup plan so you aren't completely starving. You should start when you are young. If you put in $5,000 dollars in when you are 25, the day you turn 65 that money will be worth $33,523, assuming a modest 5% a year of gains! So lets recap

- If your employer offers 401k matching, make sure you contribute the minimum to get that money.

- It might not make sense to put a whole lot of money in here, but try to stash away a little each year, you'll be grateful in the future.

Traditional Vs. Roth

Now comes the hard part! You have the option on making your contributions either Traditional or Roth. These accounts are tax advantaged because you don't pay capital gains on them, but you still have to pay income tax on the money you make! You just have the option of getting taxed now on the income, or getting taxed later.

Lets say you make $60,000 a year. The tax rate for income between $48,476 to $103,350 is 22%. So if you put $10,000 into a traditional 401k, your taxable income drops to $50,000 a year, and your tax bill for 2025 is reduced by $2200 a year.

To explain this write out the equation [(1 - tax rate)*income] * [(1 + return rate)^ years] show you can re arrange to income * [(1 + return rate)^ years] * [(1 - tax rate)] and it equal the same thing. And since its equal the same thing if you tax it later, it also means if you tax now, then have capital gains tax, thats still worse than taxing the whole thing with gains after 20 years.